Automated trading software development is where a beautiful chart meets the part of finance that bills you for being wrong. The chart gets screenshots. The order engine gets blamed.

Automated trading software development means building systems that research, test, place, monitor, and manage trades through exchange or broker APIs. A serious build includes market data, order logic, backtesting, account state, risk controls, monitoring, and audit trails. The product is not the buy button. It is everything that keeps the buy button from ruining your morning.

We have built a trading engine before, so this guide is deliberately practical: bot versus platform, exchange APIs, risk controls, backtesting, AI signals, cost, and when not to build at all.

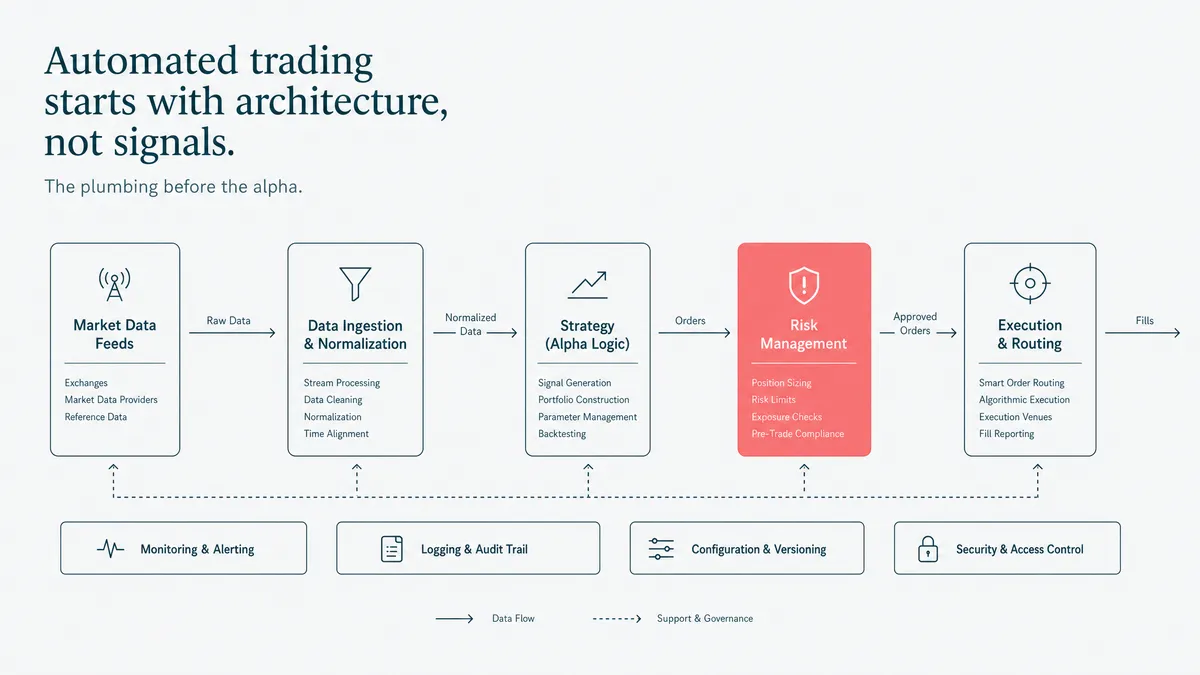

Automated trading software starts with architecture, not signals

The signal gets attention because it feels like the smart part. Sometimes it is. Often it is only the loud part.

The architecture decides whether the system survives real market behavior. A proper automated trading system needs market data ingestion, signal generation, order management, account-state reconciliation, risk checks, logging, monitoring, alerting, and a clear way to stop trading when the system is no longer sure.

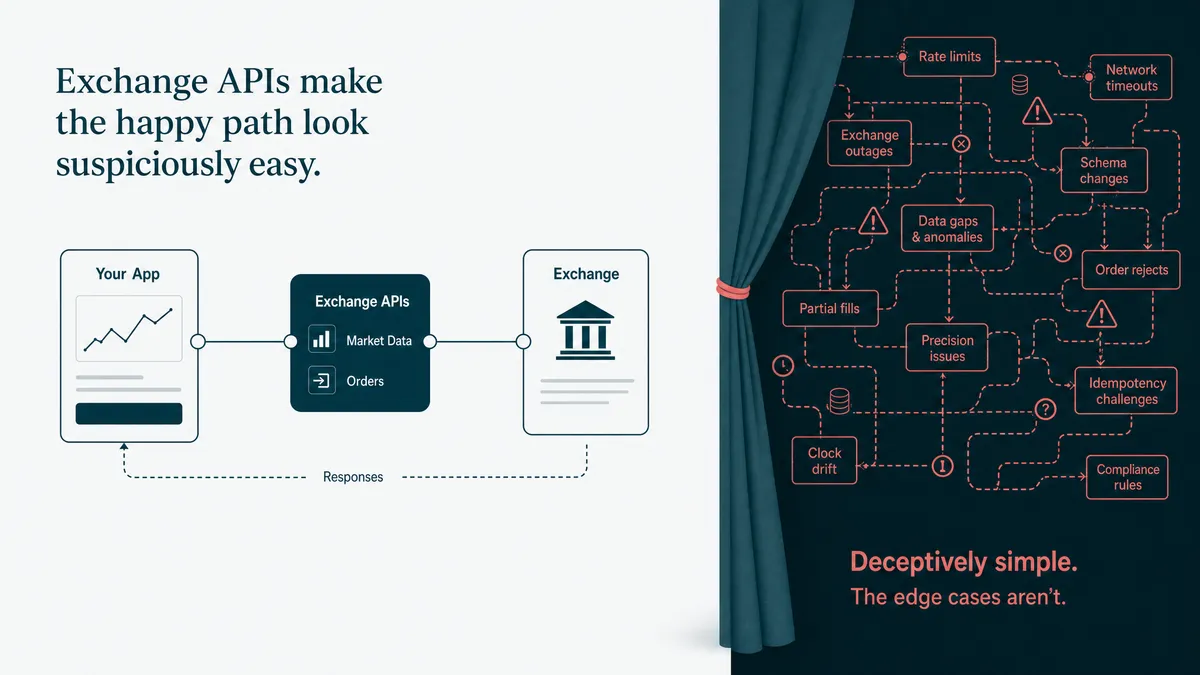

Exchange APIs do not behave like a spreadsheet. Orders can partially fill. Feeds can drop. A REST snapshot can disagree with a WebSocket event. Retries can duplicate work if idempotency is missing. A rate limit can turn a busy market into a staring contest.

Trading software development starts here: model the states and failure modes before you polish the dashboard. The dashboard can wait. The duplicate order cannot.

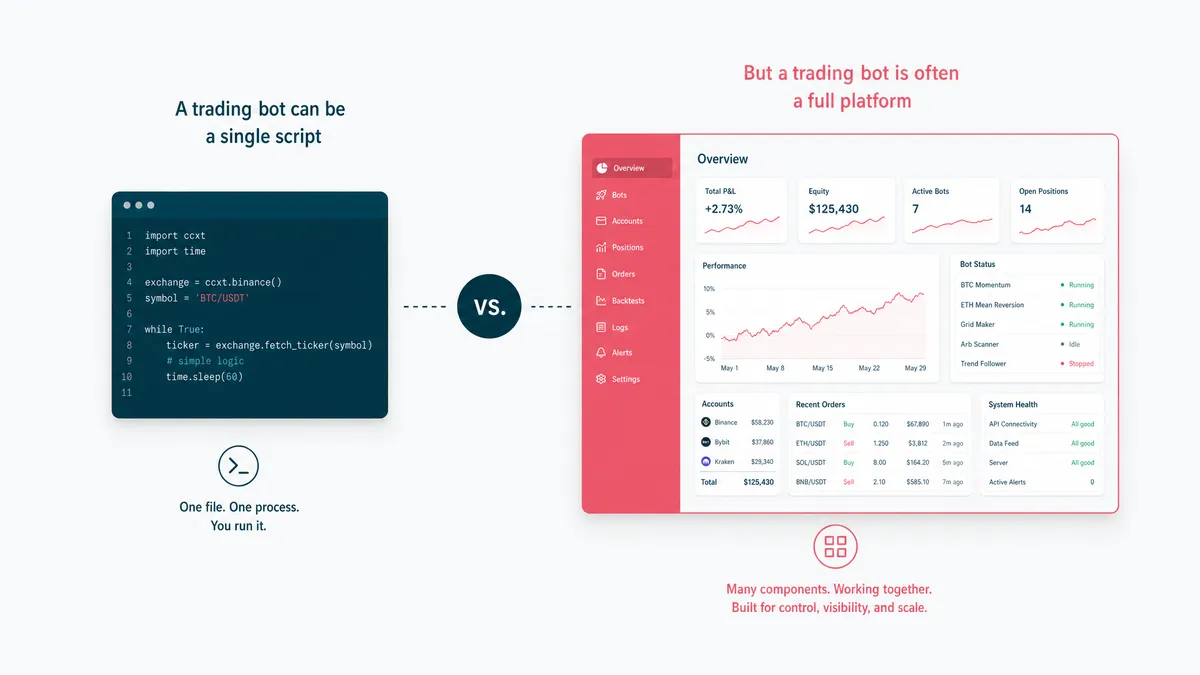

A trading bot is not always a platform

A trading bot runs a strategy. An automated trading platform runs a product.

That difference changes the build.

A bot may only need one account, one exchange, one strategy, and one operator. A platform needs users, permissions, strategy settings, audit trails, paper trading, live execution, reports, monitoring, support tools, and a way for a future engineer to understand what happened at 3:17 a.m.

The SERP for "trading bot development" is full of Reddit posts, YouTube tutorials, DIY guides, and marketplace offers. Useful for learning. Weak fit for HighCraft's buyer. We are not trying to outrank every "build a bot in Python" tutorial written after someone discovered pip install.

The better commercial wedge is automated trading software: the product layer around execution. That is where fintech software development patterns matter: money movement, correctness, access control, logs, and risk.

Exchange APIs make the happy path look suspiciously easy

An exchange API can place an order in one call. That is the demo.

The product needs everything around that call: authentication, rate limits, time sync, symbol metadata, order precision, account balances, margin mode, fills, cancellations, positions, funding, liquidation risk, retries, and reconciliation when the feed and the snapshot disagree.

The official Binance USD-M Futures API docs show the real shape: REST endpoints, WebSocket streams, limits, and account events. Broker APIs have their own shape too. The Interactive Brokers TWS API docs are a good reminder that one broker integration can be a product surface by itself.

We built Project Wolf against Binance USD-M Futures over REST and 2 WebSocket streams. The platform handled 8 order types, 9 order states, multipliers up to 125x, position-cooling lockouts, and integration tests around the dangerous parts. No fantasy latency claims. No invented trader numbers. Just the engine and the boring state logic.

That boring logic is not filler. It is where the platform earns the right to touch money.

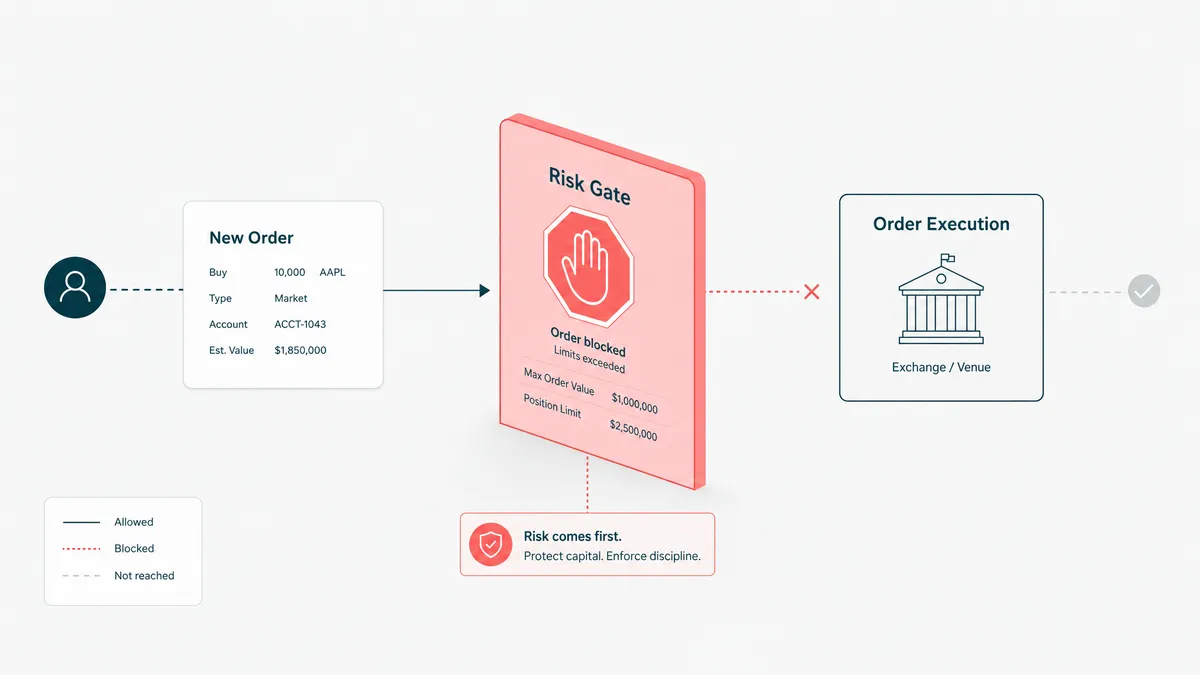

Risk controls belong before execution

Risk should not be a dashboard someone checks later. It should sit before the order leaves the system.

The basics:

- position sizing, tied to account balance and strategy limits;

- max loss checks before each allocation;

- multiplier and exposure caps;

- stop logic and exit rules;

- duplicate-order protection;

- cooling periods after a position closes;

- circuit breakers for bad data, exchange errors, and runaway signals;

- audit logs for who or what triggered the action.

In Project Wolf, every allocation validated worst-case loss against account balance before execution. That is not glamorous. It is also the kind of boring sentence you want in a trading platform. Glamour is for the chart. The risk layer is for keeping the chart from becoming a true-crime podcast.

For regulatory context, FINRA's algorithmic trading topic page is worth reading even if you are not building for a broker-dealer. It frames algorithmic trading as a supervision and control problem, not only a code problem.

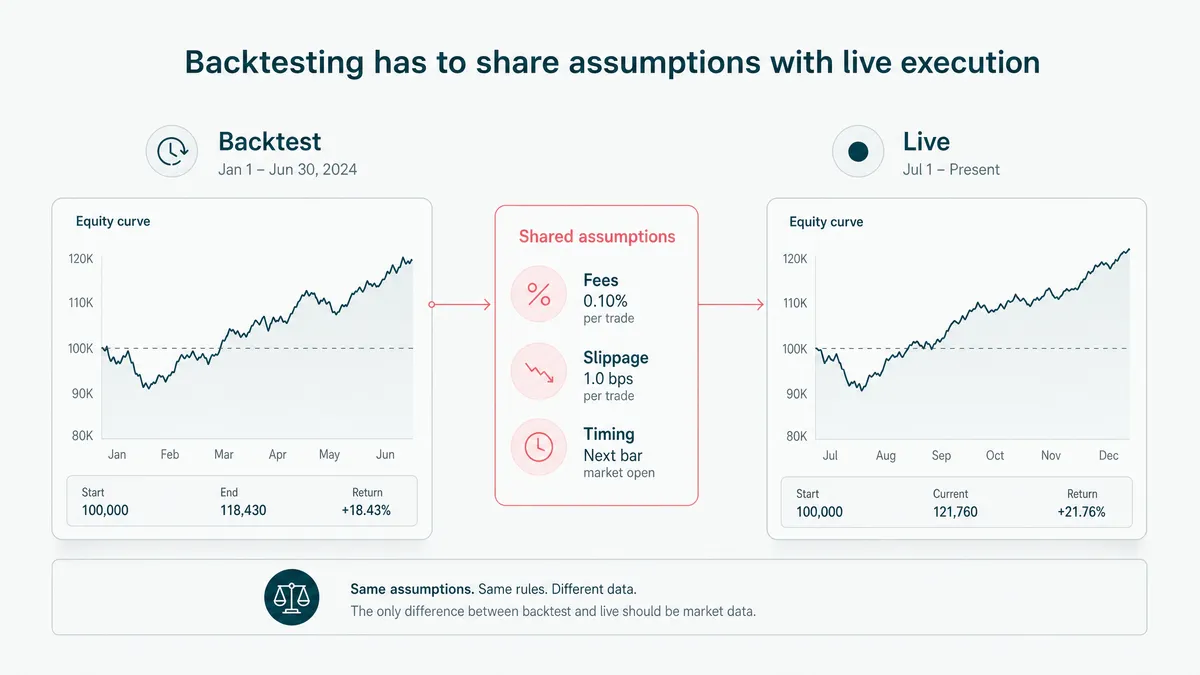

Backtesting has to share assumptions with live execution

Backtesting is useful only if it models the things live trading will charge you for.

A backtest that ignores fees, funding, slippage, liquidation, failed orders, order precision, and position state is not research. It is a compliments machine. Compliments are nice. They do not pay for bad fills.

The cleaner architecture keeps the backtester close to the live engine. Strategy logic, allocation assumptions, position sizing, symbol rules, and cost modeling should not drift into separate fantasy worlds. If research and live execution use different rules, the backtest will look better than the product. It always does. It has home-field advantage.

Project Wolf's backtester simulated funding fees and liquidation prices beside the live execution engine. That gave strategy research and execution the same vocabulary. If you are building a platform, that shared vocabulary is worth more than another chart type.

Data engineering services often sit under this layer: market data storage, trade history, feature data, reports, and monitoring streams that can be replayed when something looks wrong.

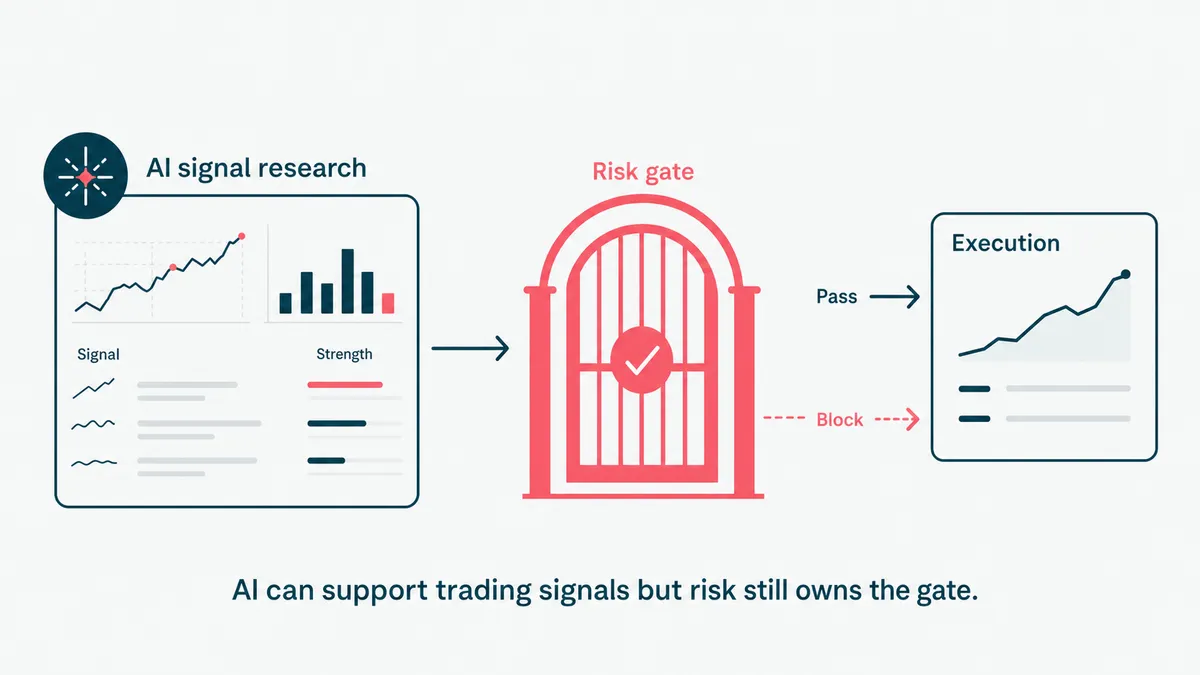

AI can support signals, but risk still owns the gate

AI can help with signal research, clustering, anomaly detection, ranking, text summaries, research assistants, and strategy-ops workflows. That is useful.

It should not become a magic box with a brokerage account.

Project Wolf used Microsoft.ML K-Means signal clustering to rank historical distributions before allocation. The model helped sort signal behavior. The platform still needed allocation rules, worst-case loss validation, position cooling, and tests. The model suggests. The risk layer decides whether the suggestion gets to speak with money.

That is also how we think about generative AI development in serious products. Context beats the prompt. A handful of good examples can improve model behavior, but examples do not replace controls. The last 10 percent from demo to product is where teams either build evaluation or start narrating excuses.

If your AI trading feature cannot explain what data it used, what confidence means, and what risk rule can veto it, do not ship it live. Put it in research mode until it earns better manners.

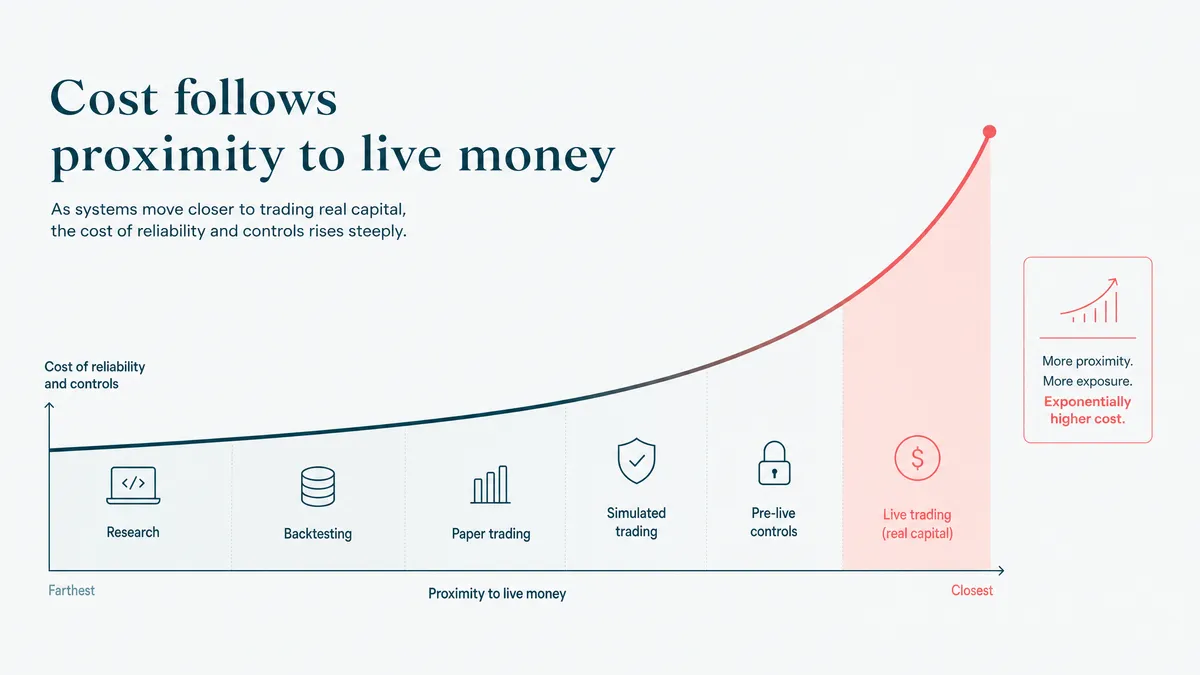

Cost follows proximity to live money

Automated trading software cost is mostly a risk and integration question.

A research prototype is one scope. A paper-trading tool is larger. A live trading platform with users, exchange APIs, account state, order execution, monitoring, alerts, logs, and support is a product. Same topic, different weather system.

The estimate moves with:

- Count the exchanges, brokers, and data providers.

- Name the order types, account modes, margin rules, and supported instruments.

- Decide whether backtesting, paper trading, and live trading share the same engine.

- Define risk controls before feature work starts.

- Decide who uses it: one operator, an internal desk, or outside customers.

- Plan monitoring, alerts, audit logs, and support tools.

HighCraft replies to project briefs with a scoped estimate in 1-2 business days. For trading software, the brief should include exchanges, instruments, order types, market data, strategy shape, risk limits, and what has to ship first.

If someone quotes a live trading platform before asking how orders fail, they are not moving fast. They are skipping the part where the money lives.

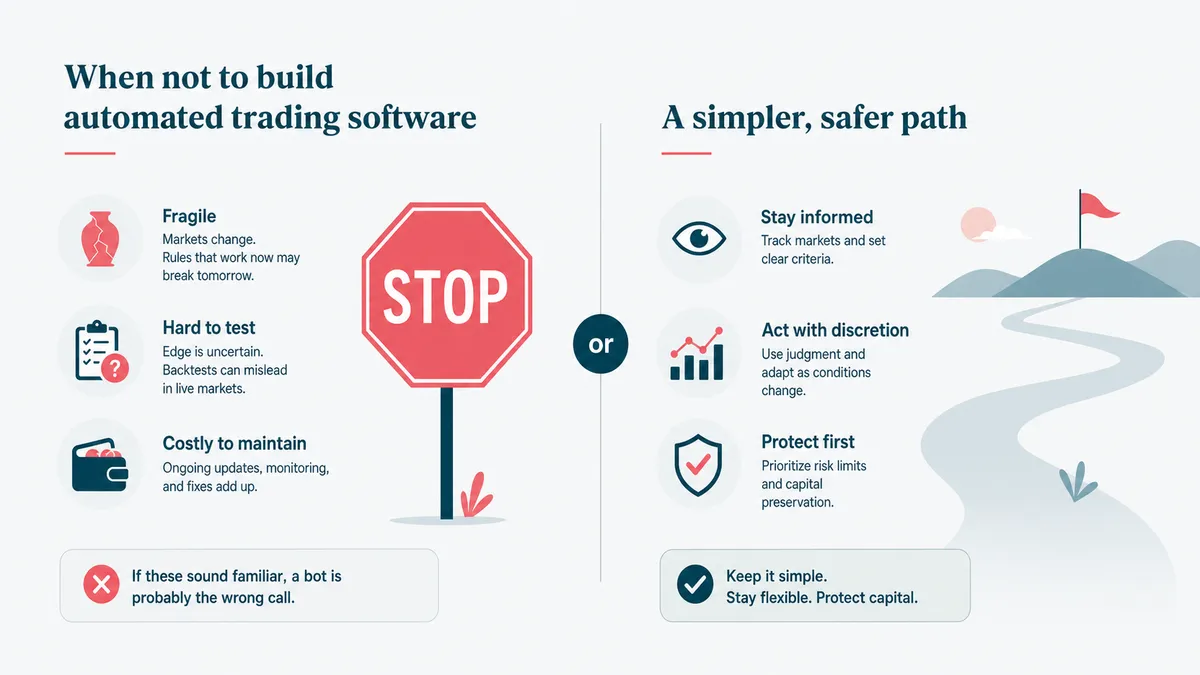

When not to build automated trading software

Do not build custom software for a simple personal bot if an existing tool or a script covers the job. Buy the tool, write the script, learn from it, and keep the budget for the part that needs engineering.

Do not build around guaranteed-return claims. We build trading software, not investment promises. If the sales deck says the model "cannot lose," the correct technical review is a long walk outside.

Do not move to live execution before backtesting, paper trading, risk limits, and monitoring have proved they can catch boring failures. Boring failures are the expensive ones. The system does not need to be cinematic to be dangerous.

Custom earns its cost when you need a maintainable product: real exchange or broker integrations, shared assumptions between research and execution, risk controls before orders, monitoring after orders, and a codebase another engineer can understand without a séance.

If that is the job, email us. We will talk about the engine first, the chart second, and the jokes only when the order state machine has calmed down.